Crypto Update & Pinterest DD

Crypto enhancements and a PINS due diligence

Swaggy’s Top Stonks. We compile and analyze data from multiple sources bringing you the top trending tickers from around the internet. If you haven’t subscribed already, please do so below.

Swaggy's Top Stonks

Together with... Defiance ETFs and the $NFTZ ETF

December 12, 2021

Welcome newcomers to Swaggy's Top Stonks and thank you for subscribing.

We've got some exciting updates coming to the SwaggyStocks website in the next 1-2 weeks. I won't give away all the sauce of what's to come, but a large part of the update will include a completely redone crypto trends section.

For those of you that aren't into crypto, not to worry because we will also be adding new sources of trending meme-stocks, a list of names popular with short-squeeze play, and a bunch more.

Today's Letter

Crypto Update

A Pinterest DD

Trending Tickers

Crypto Update

CryptoBROS (and gals). A YUGE update is coming to SwaggyStocks with enhanced social crypto trends. With all the hype around crypto and how popular it has become it's not unusual to catch some hot runners early in the trend and before they take off.

We are making a bigly push into the crypto sentiment space and it will all soon be available on the SwaggyStocks website. What it will include:

Social volume and sentiment

Hot cryptos by changes in social volume and their respective social rank

Changes in sentiment behind each of the popular coins

If you are not a crypto enthusiast then don't worry we've got a few other improvements coming to the site as well. You'll be able to take full advantage of our newly added "Short Squeeze" list that tracks the most talked about short squeeze stocks among retail investors.

Before we get into the rest of the letter here's a message from today's sponsor, Defiance ETFs and their newly launched ETF tracking the NFT industry.

Introducing NFTZ, the first NFT-focused ETF

Want to invest in NFTs, but don’t know where to start? Say hello to $NFTZ, the newly-launched ETF with a focus on all things NFT and Blockchain.

It can be confusing following the different kinds of NFT assets all on your own. Now you’re able to invest in the digital economy and gain exposure to NFTs, Blockchain, and the NFT marketplace through NFTZ.

Learn more about the fund and it’s holdings.

Due Diligence - Pinterest (PINS)

Our partner site, TheStonksHub, provided a well-written article on Pinterest and their potential outlook. Today we'll be featuring the entire article, for free. Take advantage of their holiday discount code and subscribe to the premium version of the newsletter for as little as $7/month, only $2 per article.

PINS at a glance

PINS is a social media platform that categorizes themselves as a “visual discovery engine” (source). They have built a community to share ideas ranging from wedding décor all the way to dinner recipes. These ideas are shared through bite-sized pictures and then bookmarked through a feature called pinning. PINS earns their revenue via advertising through promoted pins. Promoted pins is content that looks user-generated but is actually an advertisement paid for by a corporation (source).

The social media industry

Social media advertising

Social media advertising, in 2020 was projected to be $85B globally. By 2027, it is expected to grow to $248B at a CAGR of 16.5% (source). Much of this growth will be captured by China and India.

India is expected to be the fastest growing markets for social media advertising, growing at a CAGR of 19% (source). Already, 30% of all India’s marketing spend (the highest spend in advertising) is in social media advertising (source). As social media advertising continues to grow in India, much of this growth will be captured by American-based companies because unlike China, India has few popular homegrown social media applications. Instead, they are much more reliant on US-based social media products such as Facebook and Pinterest (source).

Social networking sites

Social media platforms, like their counterpart industry in advertising, is also expected to grown in valuation globally. They are projected to grow from $192B in 2019 to $939B in 2026 with a CAGR of 25% (source). This rise in valuation is driven by increased adoption from not just millennials but from all age groups. A few factors attribute to this growth (source):

The proliferation of smart phones is also leading to increased social media usage.

Advancements in data collection on social media users

Discovery of new usages for social media data

Increased reliance on digital marketing to lead users into a digital sales experience. For example, 70% of Chinese Generation Z shop directly from social media (source)

The financials

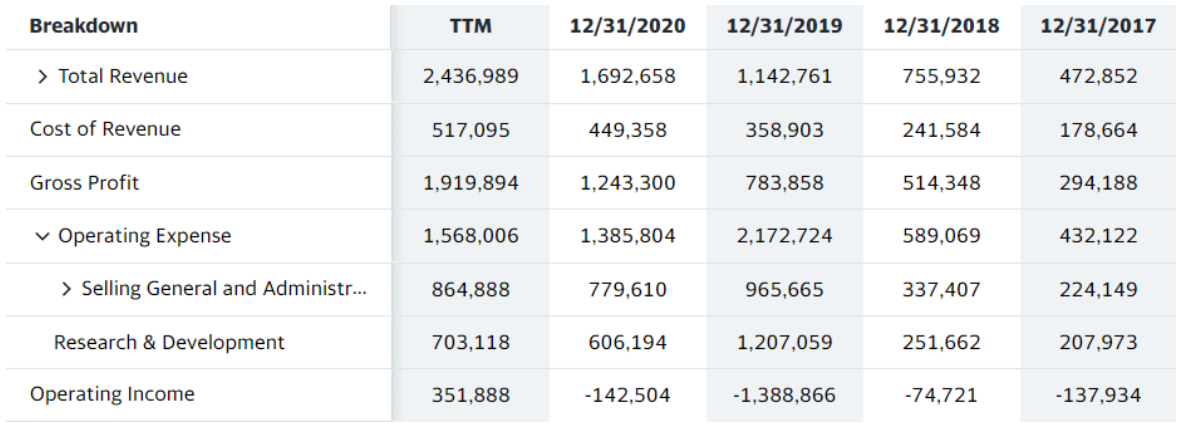

Income statement

PINS has yet to post a profit, but is very likely to post one this year. Already they have had profitable very profitable quarters. The majority of their profits is coming from operational revenues growing beyond their cost of revenues and operating expenses. So far, 2021 is looking like the first year where operating expenses only account for 60% of the total revenue generated. Hopefully this trend will continue through 2022 and PINS will further maximize operating income by reducing their operating expenses.

One quick callout on this income statement is that PINS marketing expenses has remained relatively flat in the past three years while their total revenues are growing. This may indicate that PINS has switched from trying to acquire as many users as possible and are now focusing more on making their business model more efficient.

Balance sheet

PINS has an extremely healthy balance sheet. As an internet-based company, they have little need for large asset-heavy investments such as equipment and factories. They have also consistently grown their current assets year-over-year so that they are now sitting at a ridiculously high current ratio (their current assets divided by their current liabilities). A high current ratio indicates a healthy balance sheet, but also that they may have too much cash and other liquid assets on hand and not enough opportunity to reinvest these assets into revenue growing operations.

The health of their balance sheet has led to them not needing additional financing through investments. While their number of shares issued has increased, this is not due to an issuance and more likely due to the natural inflation of shares through internal incentive programs.

Statement of cash flows

A healthy income statement and healthy balance sheet usually leads to a healthy statement of cash flows as well and this is what we see with PINS. While they were bleeding cash when they were operating at a loss, the bleeding was not so great as to put their balance sheet in jeopardy. The previous year, they actually managed to be cash positive and this year, their free cash flows may summit all their previous cash losses from the past 4 years.

Where PINS stands

The bull case

PINS is a company that operates within a very fast-expanding industry. The majority of the growth of the social media industry will come from emerging economies such as China and India. PINS understands this and during Q1 of 2021, they posted 30% growth in international monthly active users (MAU). While this growth has slowed to 9% the next quarter, these still compound into very competitive year-over-year growth rates (source). Beyond that, in Q2 2021, they managed to increase global revenue per user by 89% (source). Their global MAU growth rates far outstrip their domestic MAU growth rates indicating that they are hyper focused on global growth as a strategy (source).

As discussed in their financials, their commitment to optimize their business model can be seen through their current strategic plays as well. Catalog uploads to make their platform more shoppable increased by 50% in Q2 2021 (source). Much of their platform investment comes in automating their advertising experience to make it easier to onboard corporations who want to advertise through their platform (source).

PINS is future-oriented, deriving most of their user growth from Gen Z and millennials (source).

2021 looks to be a very promising year for PINS. They will turn an annual profit for the first time in their history while optimizing their revenue generation on the userbase they currently have. Meanwhile, they are acquiring global users at a remarkable rate and already looking at increasing the revenue generation capabilities from that demographic.

The bear case

PINS has increased their users from 265M in 2018 to 450M in Q2 of 2021, peaking at 480M in Q1. The worry here, is that they peaked (source). Social media platforms live and die by their popularity and declining MAUs may indicate a worrisome trend. Even more worrisome, PINS expects MAUs to still decline coming into Q3 2021 (source). To expand on this, most of the MAU decline is expected to come from US users which are PINS most revenue generating user group. Thus, this decline is expected to hurt PINS future revenue generation (source). While PINs is losing users, they are already far weaker in generating revenue than their peers. On average, Snapchat generates 3x the revenue per user than PINS and Meta generates almost 10x the revenue per user versus PINS (source). If PINS cannot stemmy their loss of users or figure out how to generate more revenue from these users without alienating them, they will not be able to justify their current valuations.

The verdict

While MAU decline is worrisome, there’s no indication that this marks a long-term trend. Furthermore, while PINS has not been able to generate much revenue from its users, this only represents possibility for it to further optimize their business model which they are trying to do. If they can successfully, get to even Snapchat’s revenues per user, their stock price – even with a declining MAU base – will explode. Lastly, those worried about the future of PINS platform usage should recognize that the majority of PINS growth is coming from the next generation of users. Furthermore, nearly half of PINS users have over $100K of income making their current demographic very attractive for revenue generation (source).

Disclosure: The author of this article is long PINS.

Enjoyed the read? Take advantage of TheStonksHub discount before prices go back up after the holidays.

WallStreetBets - Most Mentioned Equities

Disclaimer: All material presented in this newsletter is not to be regarded as investment advice, but for general informational purposes only. You are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer.